Aluminium-Free High-Barrier Films Market to Reach USD 3.82 Billion by 2035 as Sustainable Packaging Replaces Foil-Based Structures

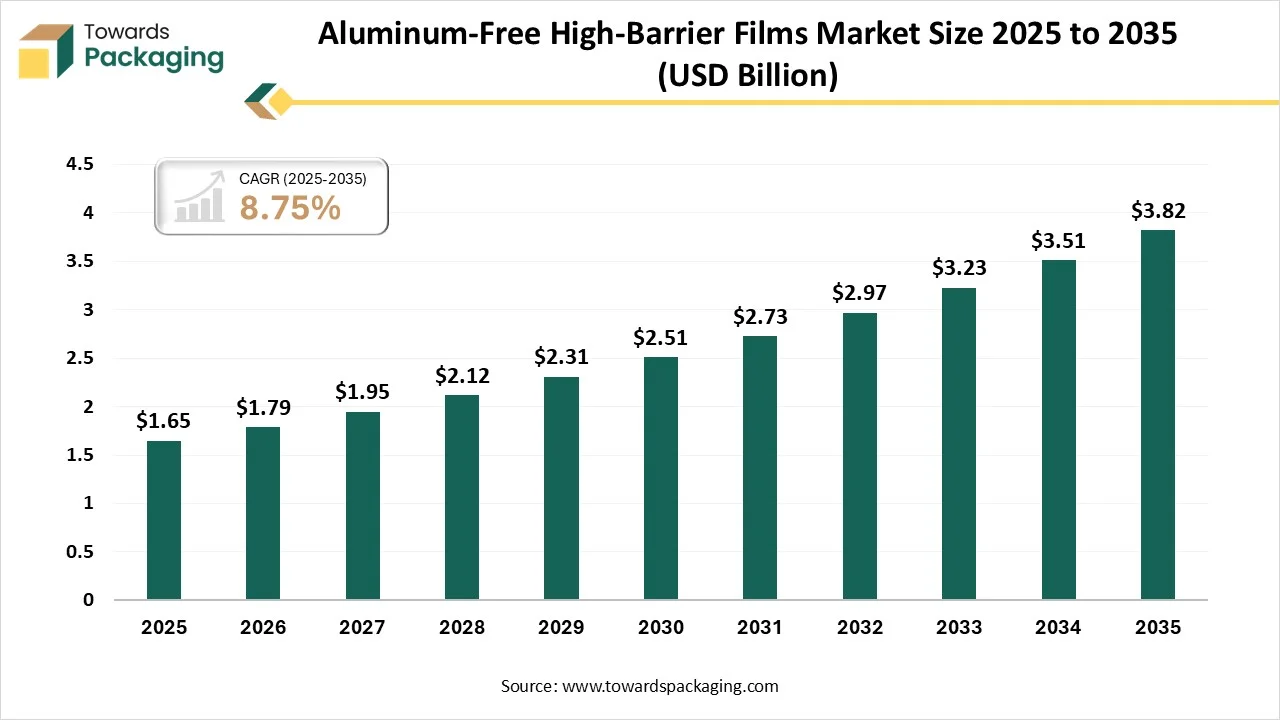

As per market analysts at Towards Packaging, the global aluminum-free high-barrier films market is expected to grow from USD 1.79 billion in 2026 to nearly USD 3.82 billion by 2035, registering a CAGR of 8.75% between 2026 and 2035.

Ottawa, March 02, 2026 (GLOBE NEWSWIRE) -- The global aluminum-free high-barrier films market size stood at USD 1.65 billion in 2025 and is projected to reach USD 3.82 billion by 2035, according to a study published by Towards Packaging, a sister firm of Precedence Research.

Request Research Report Built Around Your Goals: sales@towardspackaging.com

What are Aluminium-Free High-Barrier Films?

Aluminium-free high barrier films are advanced packaging materials designed to provide strong protection against moisture, oxygen, aroma, and light without using aluminum foil layers. These films typically use high-performance polymers and coating technologies to achieve barrier properties while remaining recyclable or lightweight.

Market growth is driven by sustainability regulations, rising demand for recyclable mono-material packaging, food safety requirements, and brand commitments to reduce carbon footprint and improve circular packaging solutions.

Private Industry Investments for Aluminium-Free High-Barrier Films:

- Mondi Group (€16 Million Investment): Mondi invested €16 million in its Solec plant in Poland to scale the production of FunctionalBarrier Paper Ultimate, an ultra-high barrier paper-based solution designed to replace unrecyclable aluminium-based structures.

- Toppan (Acquisition of Sonoco’s Packaging Business): In late 2024, Toppan agreed to acquire Sonoco’s thermoformed and flexibles business for USD 1.8 billion to significantly boost its global capacity for high-barrier films, including transparent alternatives to aluminium foil.

- Constantia Flexibles (MDO Line Investment): The company invested over €6 million in a new Machine-Direction Orientation (MDO) line at its Pirk facility in Germany to produce EcoLamHighPlus, a recyclable mono-material film that provides high-barrier protection without metal layers.

- Jindal Poly Films (₹700 Crore Expansion): Its subsidiary, JPFL Films, is investing over ₹700 crore in Nashik, Maharashtra, to add advanced packaging film lines focused on high-barrier metallized and speciality films that serve as sustainable replacements for aluminium foil.

-

Huhtamaki (Mono-Material Technology Deployment): Huhtamaki has invested in new global production technologies to launch mono-material flexible packaging in paper, PE, and PP, specifically engineered to eliminate the need for aluminium layers while maintaining retort-grade barrier properties.

What Are the Latest Key Trends in the Aluminium-Free High-Barrier Films Market?

1. Shift to Recyclable Mono-Material Structures

Manufacturers are developing aluminum-free films made from single polymer types (mono-materials) that are easier to recycle. These films maintain high barrier performance while meeting sustainability demands from brands and regulators focused on reducing mixed-material waste.

2. Adoption of Bio-Based & Compostable Polymers

There is growing use of bio-derived and compostable high-barrier materials to reduce reliance on fossil-based plastics. These innovations appeal to eco-conscious consumers and support corporate commitments to lower environmental impact across packaging lifecycles.

3. Enhanced Barrier Coating Technologies

Advanced coating methods like nanolayer and plasma coatings are being employed to improve oxygen and moisture resistance without aluminum. These technologies enable lighter films with superior performance for food and sensitive product packaging.

4. Integration with Smart & Active Packaging

Aluminum-free films are being integrated with active components such as oxygen scavengers, antimicrobial layers, or freshness indicators. These multifunctional solutions enhance product shelf life and safety while avoiding traditional foil barriers.

5. Expansion in Ready-Meal & Fresh Food Segments

Demand for ready meals, fresh meats, and chilled foods is rising because aluminum-free films offer excellent protection while enabling microwaveability and consumer convenience. Brands are adopting these films to meet clean-label and convenience trends.

What is the Potential Growth Rate of the Aluminium-Free High-Barrier Films Industry?

The aluminium-free high-barrier films industry holds strong growth potential as sustainability continues to reshape packaging priorities across industries. Brands are moving away from traditional foil-based structures due to recyclability challenges, creating demand for high-performance polymer films that offer similar barrier protection without aluminum. Growth is supported by increasing regulatory pressure for recyclable and mono-material solutions, particularly in food and pharmaceuticals.

Technological advancements in coating and multi-layer extrusion enhance performance, while growing consumer preference for eco-friendly packaging accelerates adoption. Expansion of e-commerce and convenience foods further boosts demand, positioning aluminum-free barrier films as a strategic solution for future-focused packaging portfolios.

Get All the Details in Our Solutions - Access Report Sample: https://www.towardspackaging.com/download-sample/5968

Regional Analysis:

Who is the leader in the Aluminium-Free High-Barrier Films Market?

Europe dominates the market due to stringent sustainability regulations and advanced recycling infrastructure that encourage the adoption of recyclable packaging solutions. Strong consumer demand for eco-friendly products and early implementation of plastic reduction policies further drive market preference for aluminum-free films. Additionally, well-established food processing and pharmaceutical industries support large-scale usage and innovation in barrier film technologies.

UK Aluminium-Free High-Barrier Films Market Trends

In the UK, manufacturers are actively redesigning high-barrier films to eliminate aluminum layers and improve recyclability within existing plastic recovery streams. Companies are investing in advanced coating technologies and high-performance polymers that deliver strong oxygen and moisture protection without compromising flexibility.

There is also a growing focus on lightweight film structures to reduce material usage. Collaboration between converters, retailers, and food brands is accelerating the shift toward circular, aluminum-free packaging formats.

How is the Opportunistic is the Rise of the Asia Pacific in the Aluminium-Free High-Barrier Films Industry?

The Asia-Pacific region is emerging as a key opportunity hub for aluminum-free high-barrier films due to rapid expansion in packaged foods, e-commerce, and pharmaceutical sectors. Local manufacturers are increasingly adopting recyclable, aluminum-free structures to meet tightening environmental policies in countries like China and India. Investment in advanced film extrusion and coating technologies, along with rising consumer awareness of sustainable packaging solutions, is accelerating adoption and regional production capacity growth.

China Aluminium-Free High-Barrier Films Market Trends

China’s rapid growth in the market is driven by its large manufacturing base, strong polymer production capabilities, and increasing demand from food and pharmaceutical packaging industries. Local film producers are investing in advanced barrier technologies and collaborative R&D with global partners. Growing environmental policies and emphasis on recyclable mono-material solutions have encouraged domestic innovation, while fast expansion of e-commerce and convenience food sectors further boosts demand for sustainable high-barrier films.

More Insights of Towards Packaging:

- Canada Multilayer Flexible Packaging Market Size and Segments Outlook (2026–2035)

- U.S. Pharmaceutical Packaging Services Market Size and Segments Outlook (2026–2035)

- Polypropylene Foam Trays Market Size and Segments Outlook (2026–2035)

- North America Flexible Plastic Packaging Market Size, Trends and Competitive Landscape (2026–2035)

- PET Shrink Film Market Size, Segments and Competitive Analysis 2025-2035

- Recycle-Ready Packaging Market Size, Trends and Regional Analysis (2026–2035)

- PVDC-Free Packaging Solution Market Size, Trends and Competitive Landscape (2026–2035)

- Thermoformed Trays Market Size, Trends and Segments (2026–2035)

- Ready-To-Drink Packaging Market Size, Trends and Regional Analysis (2026–2035)

- Modified Atmosphere Packaging (MAP) Market Size and Segments Outlook (2026–2035)

- North America Healthcare Flexible Packaging Market Size, Demand and Trends Analysis

- North America Amber Glass Packaging Market Size, Trends and Regional Analysis (2026–2035)

- Automated Bagging Solutions Market Size and Segments Outlook (2026–2035)

- U.S. Packaging Market Size, Trends and Segments (2026–2035)

- Pharmaceutical Packaging Laminates Market Size, Trends and Segments (2026–2035)

- Barrier Coatings for Flexible Packaging Market Size, Trends and Segments (2026–2035)

- Contoured Bottles and Containers Market Size and Segments Outlook (2026–2035)

- Diaper Packaging Market Size, Trends and Competitive Landscape (2026–2035)

- Pouch Materials for Pharmaceutical Market Size and Segments Outlook (2026–2035)

- Polypropylene Containers Market Size, Trends and Segments (2026–2035)

Segment Outlook

Film Type / Material Type Insights

The multilayer co-extruded barrier films (no aluminum) segment dominates the aluminum-free high-barrier films market because it delivers superior protection against oxygen, moisture, and aroma without relying on aluminum. Its layered structure allows customization for specific applications, meeting diverse food and pharmaceutical packaging needs. Manufacturers favour this technology for its balance of performance, recyclability, and compatibility with existing production lines, driving widespread adoption across industries.

The bio-based / compostable barrier films segment is expected to be the fastest-growing in the market because brands and consumers increasingly prioritise circular, waste-reducing solutions. These films offer strong protection while breaking down more readily after use, aligning with eco-friendly packaging goals. Growing demand from sustainable food, retail, and personal care sectors further accelerates the adoption of compostable high-barrier structures.

Barrier Technology Insights

The EVOH (ethylene-vinyl alcohol)-based barrier segment dominates the aluminium-free high-barrier films market because EVOH offers exceptional oxygen and aroma barrier properties without metal layers. Its compatibility with multi-layer co-extrusion structures makes it ideal for food and pharmaceutical packaging. High performance, processing versatility, and the ability to maintain product freshness and shelf life drive its widespread adoption across diverse industries.

The SiOx / AlOx coatings (non-aluminum oxide) segment is expected to be the fastest growing in the market because these ultra-thin inorganic layers significantly enhance oxygen and moisture resistance without adding bulk or metal. They enable high clarity and film flexibility while maintaining excellent barrier performance suitable for sensitive food and pharmaceutical packaging. Advancements in scalable coating technology and increasing demand for recyclable, high-performance films further accelerate adoption.

Packaging Format Type Insights

The pouches segment dominates the aluminium-free high-barrier films market due to its lightweight structure, material efficiency, and strong shelf-life performance. Pouches require less packaging material compared to rigid formats, reducing transportation and production costs. Their flexibility, resealability, and compatibility with high-barrier mono-material films make them highly preferred for food, pet food, and pharmaceutical applications, driving widespread industry adoption.

The lidding films segment is expected to grow at fastest CAGR in the market due to rising demand for recyclable tray-based packaging in fresh food, dairy, and ready-meal applications. These films provide strong oxygen and moisture protection while offering peelability and sealing performance. Increasing adoption of mono-material trays and MAP (modified atmosphere packaging) solutions further supports aluminum-free high-barrier lidding film demand.

End-User Industry Insights

The food & beverage segment dominates by end-use in the aluminium-free high-barrier films market due to rising demand for extended shelf life, product safety, and sustainable packaging formats. Aluminum-free films provide strong oxygen and moisture barriers required for snacks, ready meals, dairy, and processed foods. Growing preference for recyclable mono-material packaging and convenience-based consumption patterns further strengthens this segment’s leading position across retail and e-commerce channels.

The pharmaceutical & healthcare is expected to be the fastest growing segment in the market due to strict product protection requirements and increasing demand for sustainable medical packaging. These films provide excellent moisture and oxygen barriers essential for sensitive drugs and medical devices. Rising regulatory focus on recyclable materials, growth in generic drug production, and expanding healthcare access globally are accelerating adoption of advanced aluminum-free barrier film solutions.

Recent Breakthroughs in Aluminium-Free High-Barrier Films Industry

- In February 2026, Pomurske Mlekarne, a Slovenian dairy producer, has partnered with SIG to offer its milk in aluminum-free aseptic cartons. SIG's Terra MidiBloc Alu-free + has been added to Pomurske Mlejko 2.8% low-fat milk since its relaunch complete barrier packaging. The recently adopted carton uses a thin polymer coating in place of the traditional aluminum layer to shield the product from light, oxygen, moisture, and odor loss.

- In September 2025, TIPA Compostable Packaging expanded its portfolio with four new high-barrier film and laminate products suitable for single-serve and flexible packaging. These aluminum-free, compostable films provide moisture and oxygen barriers comparable to conventional packaging while remaining compatible with existing machinery, enabling brands to protect products sustainably without sacrificing performance.

Top Companies in the Global Aluminium-Free High-Barrier Films Market & Their Offerings:

Tier 1:

- Amcor PLC: The AmLite line uses a transparent silicon oxide coating to provide foil-level protection in a metal-free, recyclable structure.

- Berry Global Group, Inc.: Their HiBloc co-extruded films offer high moisture barriers and allow for metal detection by replacing traditional foil layers.

- Coveris Holdings S.A.: The MonoFlex range utilizes high-performance EVOH barriers in mono-material films to eliminate the need for aluminum in flexible packaging.

- Cosmo Films Ltd.: They produce specialized Transparent High Barrier Films that use proprietary coatings to replace three-layer aluminum laminates with simpler, non-foil structures.

- Sealed Air Corporation: Their CRYOVAC barrier films use multi-layer polyolefin technology to deliver superior oxygen and aroma protection without metal.

- Mondi Group: The FunctionalBarrier Paper Ultimate is a fiber-based solution that uses a unique functional coating to replace aluminum-plastic laminates.

Tier 2:

- Huhtamaki Oyj

- Toray Plastics Co., Ltd.

- Uflex Limited

- ProAmpac (THX Group)

- Klöckner Pentaplast Group (K-P)

- Winpak Ltd.

- Innovia Films

- LINPAC Packaging

Segment Covered in the Report

By Film Type / Material

- Polyamide (PA)-based High-Barrier Films

- Polyethylene (PE) + Barrier Co-polymers

- Polyethylene Terephthalate (PET)-based Barrier Films

- Polyolefin Barrier Films (PO)

- Bio-based / Compostable Barrier Films

- Multilayer Co-extruded Barrier Films (no aluminum)

By Barrier Technology

- EVOH (Ethylene Vinyl Alcohol)-based Barriers

- SiOx / AlOx Coatings (non-aluminum oxide)

- Nanocomposite / Nano-clay Barrier Films

- PLA & Bio-polymer Barrier Systems

By Packaging Format

- Pouches (stand-up, flat, zipper)

- Lidding Films

- Shrink / Stretch Films

- Wraps & Bags

- Vacuum / MAP (Modified Atmosphere Packaging) Films

By End-Use Industry

- Food & Beverage

- Snacks & Ready-to-Eat

- Meat, Poultry & Seafood

- Bakery & Confectionery

- Dairy & Cheese

- Frozen Foods

- Pharmaceutical & Healthcare

- Personal Care & Cosmetics

- Industrial / Specialty Packaging

By Region

North America:

- U.S.

- Canada

- Mexico

- Rest of North America

South America:

- Brazil

- Argentina

- Rest of South America

Europe:

- Western Europe

- Germany

- Italy

- France

- Netherlands

- Spain

- Portugal

- Belgium

- Ireland

- UK

- Iceland

- Switzerland

- Poland

- Rest of Western Europe

Eastern Europe

- Austria

- Russia & Belarus

- Türkiye

- Albania

- Rest of Eastern Europe

Asia Pacific:

- China

- Taiwan

- India

- Japan

- Australia and New Zealand,

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

MEA:

- GCC Countries

- Saudi Arabia

- United Arab Emirates (UAE)

- Qatar

- Kuwait

- Oman

- Bahrain

- South Africa

- Egypt

- Rest of MEA

Invest in Our Premium Strategic Solution: https://www.towardspackaging.com/checkout/5968

Request Research Report Built Around Your Goals: sales@towardspackaging.com

About Us

Towards Packaging is a global consulting and market intelligence firm specializing in strategic research across key packaging segments including sustainable, flexible, smart, biodegradable, and recycled packaging. We empower businesses with actionable insights, trend analysis, and data-driven strategies. Our experienced consultants use advanced research methodologies to help companies of all sizes navigate market shifts, identify growth opportunities, and stay competitive in the global packaging industry.

Stay Connected with Towards Packaging:

- Find us on Social Platforms: LinkedIn | Twitter | Instagram | Threads

- Subscribe to Our Newsletter: Towards Sustainable Packaging

- Visit Towards Packaging for In-depth Market Insights: Towards Packaging

- Read Our Printed Chronicle: Packaging Web Wire

-

Get ahead of the trends – follow us for exclusive insights and industry updates:

Pinterest | Medium | Tumblr | Hashnode | Bloglovin | LinkedIn – Packaging Web Wire | Globbook | Substack | Bluesky | Justdial | Crunchbase | TrustPilot | Bizcommunity - Contact: APAC: +91 9356 9282 04 | Europe: +44 778 256 0738 | North America: +1 8044 4193 44

Our Trusted Data Partners

Precedence Research | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Healthcare Webwire | Packaging Webwire | Precedence Research Insights

Towards Packaging Releases Its Latest Insight - Check It Out:

Cohesive Packaging Market Size, Trends and Competitive Landscape (2026–2035)

Recyclable mono-material PE Market Size, Trends and Competitive Landscape (2026–2035)

Sustainable Wipe Packaging Market Size and Segments Outlook (2026–2035)

Tobacco Packaging Market Size and Segments Outlook (2026–2035)

Europe Pharmaceutical Packaging Materials Market Size, Trends and Competitive Landscape (2026–2035)

North America Tin Cannabis Packaging Market Size and Segments Outlook (2026–2035)

Semi-Automatic Stretch Wrappers Market Size, Trends and Competitive Landscape (2026–2035)

Cut Flower Packaging Market Size, Trends and Segments (2026–2035)

Clear Plastic Film Market Size, Trends and Competitive Landscape (2026–2035)

Edible Packaging Market Size, Trends and Regional Analysis (2026–2035)

Glass Packaging Market Size, Trends and Regional Analysis (2026–2035)

U.S. Rigid Thermoform Plastic Packaging Market Size, Trends and Segments (2026–2035)

Canada Plastic Packaging Market Size, Trends and Regional Analysis (2026–2035)

Packaging in Supply Chain Management Market Size, Trends and Segments (2026–2035)

North America Food Packaging Market Size, Trends and Segments (2026–2035)

North America Blister Packaging Market Size, Trends and Regional Analysis (2026–2035)

![]()

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.